Stocks Look for Seasonal Strength

As reported in the past few missives on the subject, stocks, and bonds have been having a generally tough time.

We warned that this was going to happen, and we were lucky enough to get the call right. Weakness continued through the month of October and just might extend into the first weeks or so of November.

Many assumed the recent strength was “a new bull market.” We expressed doubts, in part because of the trend in interest rates and also because valuations remain quite high. But we admit we did not anticipate how weird this market would prove to be. While the market is still nominally up for the year, only 27% of stocks in the S&P are trading above the longer-term 200-day moving average. In the case of the broader NYSE average, only 28% are above their 200-day moving average.

Can you have a bull market with almost three-quarters of the stocks within the broad equity indices heading down? Not really. What you can say is that a handful of mega-cap stocks can make the market appear to be in an uptrend, when the bulk of shares are actually going lower.

We have urged caution by suggesting more money in market-neutral cash and short-term bonds, and less money in equities and long-dated bonds. Now that short-term T-bills pay over 5%, it has been a good place to be.

During this most recent decline, results have varied depending on the time period measured and which sector of the market you may be positioned.

The best performer has been Big Tech, which is responsible for most of the gains in the S&P 500, due to the capital-weighted nature of that index. That said, indications are that this leadership is now weakening.

But QQQ, which represents the 100 largest companies in the NASDAQ is up 30% or so on the year. That looks quite good at first glance.

However, the tendency to measure results in one-year increments can be deceptive. Most indices peaked out by the spring of 2021, or a bit earlier. So, if you look at a three-year time frame, the QQQ is down about 14%. Since inflation has soared in the past three years of Bidenomics, the real performance is not as good as headlines would suggest.

The widely followed and indexed S&P is up about 11% so far this year but is down about 12% from its high reached in 2021.

However, the equal-weighted S&P, which removes the distortion of the “Magnificent Seven” big tech companies, is down about 2% so far for the year, but down 18% from its high a few years ago.

The Russell 3000 (IWV) represents smaller companies. The so-called “small cap” has been having a rough time. It is down 10% so far this year, and down about 14% from the highs three years ago. This may be because balance sheets and cash holdings are weaker for small companies and the rise in interest rates is playing havoc with their refinancing costs.

However, other sectors have soared. XLE, which represents traditional hydrocarbon energy, is up 188% over the past three years. Money managers that kicked oil stocks out of their portfolios for green/political reasons, did their investors a terrible disservice. ESG funds have generally seen large outflows and people seem finally to be souring on “woke” investing.

Sharply rising interest rates have taken a modest toll so far on equity prices but have created the worst three-year return for bonds in American history. TLT, an index that measures the value of longer-term treasury bonds is down a whopping 43.5% or so from the high reached three years ago.

Thus, with stock and bonds both struggling during the Biden period, the typical 60% equities and 40% bond allocation has been a loser, especially if measured against inflation during that period. Bottom line, most investors taking a diversified approach, have lost ground over the past three years, and largely so far this year.

Don’t be too upset with your financial advisor. They simply have not had good markets to work with and concentrated bets that have been good would have violated the prudential rules that they must abide by.

There is some hope, at least in the short term. Stocks have now become pretty oversold on a momentum basis. In addition, stocks tend to do well from Thanksgiving and into January. Of course, there is no guarantee, but that is the history.

Complicating matters, 3Q GDP was strong, suggesting the FED cannot ease back on interest rates anytime soon, which muddies the picture of the “seasonal strength” stocks usually show in the period just ahead.

In addition, the massive size of government debt issuance is putting downward pressure on bond prices, which is another way of saying interest rates are rising for market-driven reasons of supply and demand and are now out in front of the FED, which has “paused” rate increases.

Given how sharply interest rates have risen, we are a bit surprised stocks have not done worse.

It is somewhat surprising the economy likewise has done as well as it has. But it simply may be that huge fiscal stimulus has delayed the pain and that it will come in time. Interest rates on home mortgages are now breaching 8%, and real estate turnover has slowed to a crawl. Most consumers have their money tied up in their homes and it has been the consumer who has carried the economy. Also, the cash hoard the public had built up from all the “stimulus” checks has now largely been dissipated. This in turn explains the explosion in credit card debt as people try to continue to support their standard of living. But borrowing at credit card rates to maintain a standard of living is like a snake eating its tail.

Rising rates have kept the dollar strong, driving up the trade deficit and creating a headwind for gold.

Gold is up about 11% over the past three years, which is not a terrible performance given the strength of the dollar. Measured in most other foreign currencies, gold is already at new highs while in dollar terms it hovers just below old highs.

Gold is now showing better relative strength than the stock market. Given the runaway deficit spending, likely more defense spending, a probable slowdown that will force the FED to pivot, the chance of expanding war, and political chaos next year; investors may want to look seriously at gold. It is currently “oversold” and Western investors continue to bail out of gold bullion ETFs, while most central banks continue to buy gold quite aggressively. Weak hands are selling, strong hands are buying, and the public is not paying much attention to gold. Fundamentally, that is a good setup for the yellow metal.

We view gold more as insurance against political mismanagement of money, and that seems more necessary than ever.

The first gold purchases should be in the form of bullion coins or small bars. Investors should take delivery of the actual metal itself and store it safely.

Our longest-term advertiser would be a good place to start. Call American Precious Metals at 602-840-5500 or 1-800-522-GOLD. If you are inclined to buy, please support them and The Prickly Pear.

Insofar as stocks are concerned, the short-term weakness has not yet broken what we believe remains a primary bull market. However, continued deterioration has occurred with daily prices now falling below the key 200-day moving average, and shorter-term 21-day and 50-day have crossed and rolled over to the downside.

Certainly, the stock market is oversold and due to bounce. But higher interest rates are doing their damage and while the recession call by many seems to have been too early, 2024 could still see a recession emerge.

The yield curve remains inverted, but it is starting to de-invert. Market declines have often occurred during the de-inversion process.

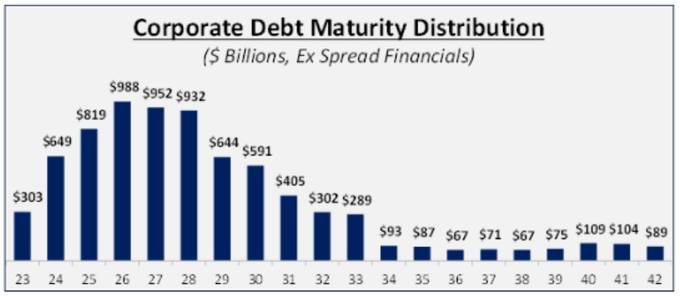

We also have growing concerns about a “credit event” that could shake markets. Years of zero or near-zero rates made use of heavy financial leverage quite popular. As rates rise, assets sensitive to rates such as bonds and mortgages decline in value. Those institutions that hold them like banks, insurance companies, finance companies, and pensions, have suffered substantial losses. We don’t really have special insight as to where the problem will reveal itself but rest assured somebody out there is taking a beating. As we are seeing in China, it is possible the credit event could start abroad and spread here or it will be of domestic origin.

This chart will give you an insight. Huge amounts of domestic corporate debt come due over the next five years and must be refinanced at much higher rates. For the marginal borrower, this is going to be painful, if not fatal.

Therefore, other than some seasonal strength and a bounce from an oversold condition, we remain cautious about heavy allocation to stocks and prefer to park in 5% plus short-term T-bills while we await more information. Stay in high-quality debt.

Much celebration has occurred because of the strong Q3 growth reported. However, those who like to parse the numbers complain that almost all the growth is attributable to huge Federal spending. Government spending is approximately 37% of GDP.

What is true though is the Friday PCE (Personal Consumption Expenditure) inflation numbers were bad, well above the FED’s 2% inflation rate. Let’s face it. The FED and Biden uncorked inflation and they can’t get it back into the bottle. The market’s hopes for lower rates look increasingly bleak.

*****

Image Credit: Shutterstock

Chart: Jesse Felder