The Peculiar Math of Market Corrections

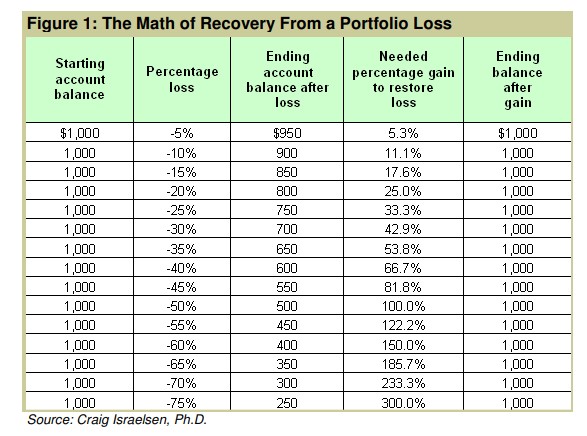

We like to call this the “peculiar math of corrections” because at first, it does not make sense. Suppose you buy a stock and it falls by 50%. If the stock comes back 50%, you will break even, right? No, if an investment falls 50%, it must come back 100%. Could that happen? Well, yes it can and has happened. Just back in the 2007-2009 financial crisis, the broad market fell by 55%, which then required the market to rise 122%, just to break even. The market did recover like that, but it takes time. The key takeaway is if you are older, and lack time, buy and hold may not work for you. If you ride into a large correction, the market must come back more than you think, and you might run out of time before the market can recover. This is a least one good reason for older investors to be more conservative. Playing the game of outperforming your neighbor is less important than preserving your capital.

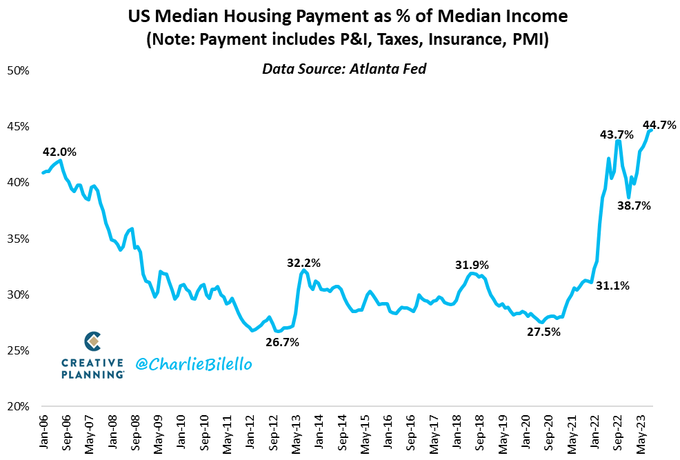

Typically financial planners don’t think housing payments should consume much more than about a third of income. The reason is that too much spent on house payments crowds out other necessary household spending. The current affordability crisis is caused by rapidly rising home prices coupled with rapidly rising interest rates to finance the mortgage. This chart shows that right now, it is taking almost 45% of median income to buy a home. While this chart only goes back to 2006, it does show that the percentage now is higher than where it was preceding the last crash in residential real estate. That does not necessarily guarantee a housing crisis, but common sense suggests when people can no longer afford to buy a home, they won’t. Demand for homes will fall unless wages suddenly rise to bring the relationship back to normal (regression to the mean). If wages don’t rise dramatically in real inflation-adjusted terms, then it is likely that housing prices have to fall, or interest rates have to fall (or both) to allow the regression to the mean to occur. Given the current economic environment, which would you wager would be the most likely outcome?

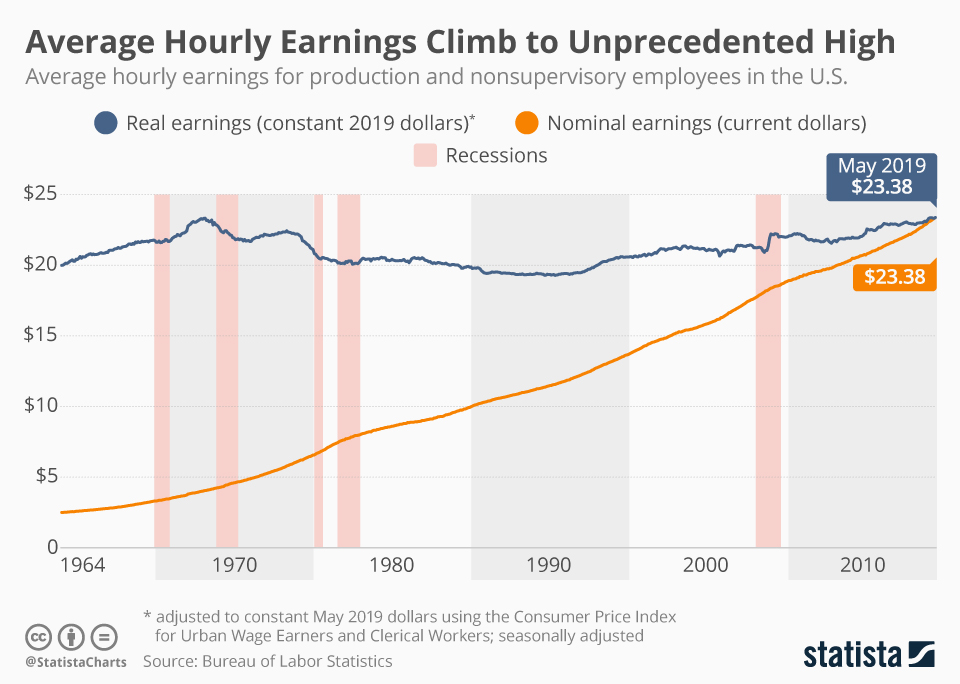

In connection with the thought above, this chart shows that since the 1960s, nominal wages have climbed substantially (the orange line), but when adjusted for inflation (the black line), they are amazingly flat. Some people say that is not all that important because, since that time, workers now receive substantial non-wage benefits (pensions, healthcare, maternity leave, etc.). This is true. However, these non-wage benefits are not available to purchase a home or to pay interest on the mortgage. For that, you need the cash flow of wages. With that in mind, the odds of a huge increase in real wages to allow home affordability to regress to the mean looks unlikely since it has not occurred during a very dynamic period of growth since the mid-1960s. Inflation caused by profligate government spending ate most of it up. Why would that suddenly change much for the better? If that is true, then interest rates and home prices need to fall so the American dream of owning a home can be realized. Perhaps new manufacturing methods and materials can be used to lower prices. Or, prices might come down as they have in the past when the economy goes into recession. Either way, lower prices and lower interest rates will be needed to allow greater affordability.

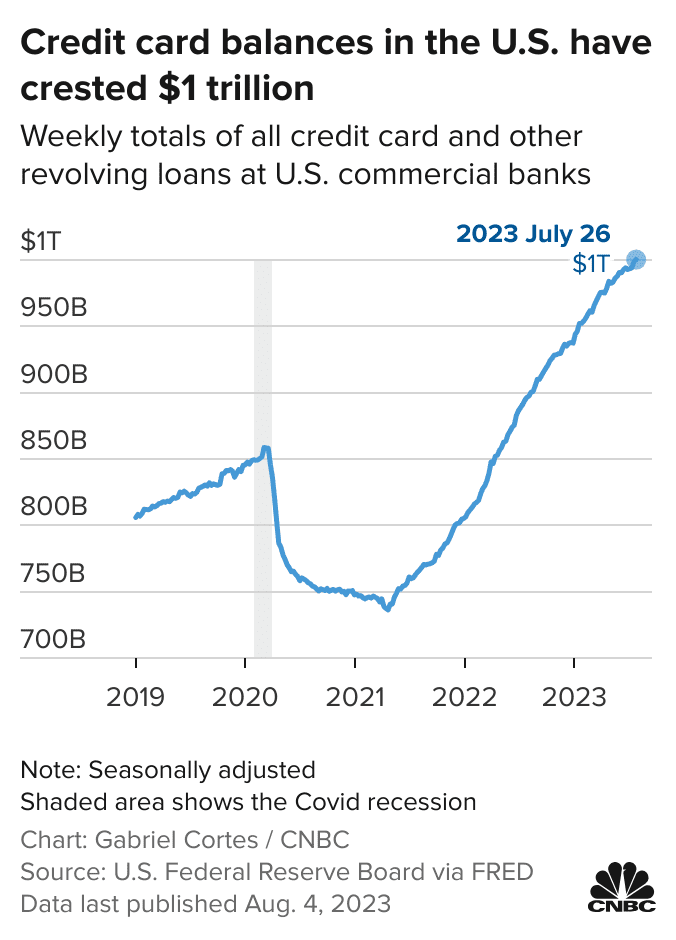

Credit card debt is rising very sharply. Some of this can be explained by the opening up of the economy after the disastrous “lockdown” policies to supposedly fight Covid. Certainly, some recovery was due. Some suggest this rise is a sign of public confidence in the future of the economy. People will tend to borrow more when they feel more confident. However, that does not square with polls that suggest only about 21% of the population feel their economic conditions have improved. Such a spike in debt may also be caused by a spike in real wages, providing more ability to go into debt. Unfortunately, as we just discussed above, a spike in real wages has not occurred recently and has not occurred going back 50 years. As with house payments, the increase in non-wage benefits cannot be used to pay down monthly credit card balances. In addition, the average interest rate on credit card balances right now is over 25%, a brutal price to pay for immediate consumption. If not real wage gains, if not tremendous economic confidence, what could be driving people to borrow so much money at punitive rates? One possible explanation is they have to, just to maintain their perceived “standard of living.” This suggests quite the opposite of confidence: economic desperation. If it is the latter, this could cause real trouble if the economy were to roll over into recession. Debt stays on the books as they say, but real wages can disappear instantly with layoffs.

Most individual investors and most professionals have not done as well as the S&P Index. That is why the craze for “indexing” has taken hold. If your manager can’t do much better than an indexed ETF, why pay all the management fees? It makes sense. However, buying an index is not a guarantee either. Over the past two years, stocks have not returned much at all. While there has been a great deal of fluctuation, after all the sound and fury, the market has been flat. Bonds have been down as well, making the standard 60% stock, and 40% bond allocation a loser in recent times. However, as the chart shows, simply rolling T-Bills and compounding the interest has beaten the market. Admittedly, this is unusual. But we live in unusual times, don’t we?

*****

Image Credit: Wikimedia Commons