Central Bank Folly and Its Repercussions

Most readers are likely familiar with discussions concerning Quantitative Easing. This was pioneered by Japan’s central bank and modified and emulated by many central banks around the world.

Its adoption by US authorities was vital as the Federal Reserve acts as the defacto central bank, of central banks. While arcane, it basically is a policy of central banks buying assets, thus expanding bank reserves, all with money created out of thin air. In that sense, it is the old technique of governments inflating their currency to pay the bills but dressed up in new fancy clothing. Many like former Federal Reserve Chairman Ben Bernanke believe it was essential as an emergency measure to stabilize an imploding economy during the financial crash of 2007-2008.

The policy seeks to achieve several things. Foremost it creates a new demand for bonds, thus lowering interest rates. It expands the reserve capital of the banking system, allowing banks to lend more freely. Finally, it helps drive up asset prices (asset inflation), which purportedly creates a “wealth effect”, supposedly stimulating the economy.

However, as you might expect bailouts want to become permanent, and monetary stimulation via QE was applied even as the economy was recovering. Easy money and zero interest rates build up a natural constituency to keep the stimulus coming. Thus, the stimulus was kept on for too long. Interest rates were kept near zero for too long.

Inexplicably, the Fed wanted to move the inflation rates from the mild 1.7% under Trump to 2%. For that incremental “benefit”, the Fed has set the world on fire. Inflation in Phoenix is the highest in the nation, nearly 13%. Thanks to the Fed and Biden, inflation is no longer 1.7%. Feel better?

Now, our own Federal Reserve is trapped, having to offload securities because of inflation, in a weak and illiquid treasury market (foreigners are no longer buying our debt), and putting upward pressure on interest rates just as the US and other nations head into a recession. It needs to raise rates to choke inflation, which means asset sales from central banks or Quantitative Tightening.

Bernanke recently won a Nobel Prize in Economics for his monetary shenanigans, which perhaps is a tragic statement of where we are with the economics profession, at least as determined by Scandanavian socialists who pass out the prize. But the US was not the only central bank doing this. Some went to even greater excess such as Japan and Switzerland, which went well beyond purchasing government bonds and mortgages to actually purchasing equities. Our friend Wolf Richter recently surveyed the difficult spot now for the Swiss Central Bank, having to sell stocks into a rather weak market.

Central banks increasingly became giant hedge funds, using newly created currency to purchase securities, thus interfering with the natural pricing structure. In fact, if such action were taken in the private sector it would be considered market manipulation, but as long as government and their central banks manipulate prices, it is supposed to be a great thing.

Ultra-low interest rates encourage both the government and private sectors to borrow excessively (free money) and use financial leverage to excess, setting the system up for a liquidity crisis, punctuated by a scramble to get liquid and pay down debt(forced asset sales). Those that can’t get liquid in time, default or go bankrupt.

It also raises serious questions about whether government agencies (central banks are independent in name only) should be shareholders in private companies, many of them foreign.

This creates a serious conflict of interest among politicians. Modern political campaigns cost a great deal of money. Politicians get most of their money mostly from “the donor class”, who are wealthy people who own assets, driven up in price by politicians. Witness the recent collapse of crypto marketer FTX, whose founder was the second largest contributor to the Democrat Party. It would be a virtuous loop if it was not such a menace to democratic government.

However, just as the US Fed is having trouble offloading its huge inventory of bonds, so the Swiss central bank is offloading stocks, into a rather weak market.

Who pays for these losses? Will this cause bank reserves to contract going into a recession? And why would the once solid bastion of monetary sanity (Switzerland) engage in such risky behavior?

It seems all the glory is in the gain during accumulation, and the pain of offloading central bank assets never entered their mind. It remains to be seen if the damage inflicted on markets and the economy by the unwinding of QE was worth the short-term benefits of QE expansion.

Why was it thought bank bureaucrats would be any better at timing stock purchases than anyone else?

It seems clear that as the current tightening of credit continues, something will break in the system. Such pain is what is needed to crush inflation, but the risk is things get out of hand.

Further, if Swiss banks and the Swiss Franc are no longer a haven for monetary stability, what is? Certainly, cryptocurrencies have been touted as the answer. However, as soon as it looked like Quantitative Easing (buying securities) was reversed to Quantitative Tapering (selling securities), cryptos went into a bear market. Quite a few have imploded together and recently even an exchange where they are traded blew up. It was worth $16 billion one day, and $1 the next.

Cryptos as a cure for monetary excess appear worse than the disease.

It is interesting that gold, which has fallen out of favor among western investors is starting to stir again, and central banks have bought more gold than at any time since 1967, just prior to the entire post-war monetary arrangments (The Bretton-Woods Treaty) falling apart. A new regime of floating currencies based on the dollar as the reserve currency emerged, and now, that regime, which lasted over 40 years, seems under severe pressure.

Indeed, the likelihood of competing systems that are not dollar centric, is forming. A group of countries (BRICS) is forming to settle payments with currencies other than the US dollar. Brazil, Russia, India, China, and South Africa, already are developing a plan, and another dozen countries have expressed an interest in joining.

Part of this is because as a reserve currency issuer, the US is abusing its privilege. Our monetary and fiscal house is out of order, and as part of our counter-attack against Russia, we seized their foreign currency reserves. Such unilateral action by the US was unprecedented. India, China, and other large countries looked and that and said, “that could be us next time.”

The big macro question is this: as central banks around the world reduce their holdings of securities, will this remove the “stimulus” which has elevated so many asset prices to ridiculous levels?

We think the answer is yes, it will.

The recent rally in world equities could rally a bit further, but we doubt their staying power into next year.

More and more indicators are coming in suggesting a recession is coming, likely next year. The interest yield curve is inverted, housing starts are faltering, housing prices are weakening, and homes are the biggest sources of wealth for American households.

Corporate earnings have been falling.

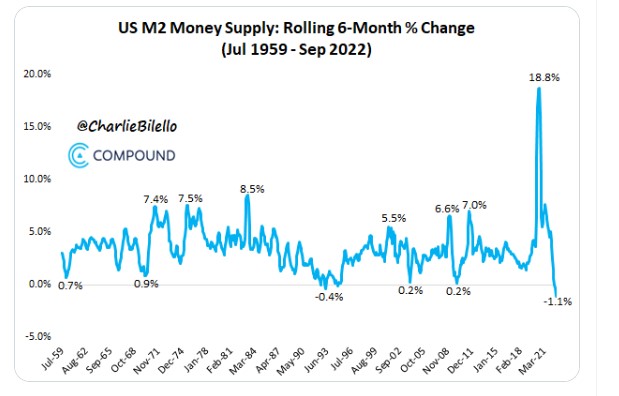

The money supply has peaked and rolled over hard. Container prices are falling.

The Leading Economic Indicators look weak and have been falling for six months.

People feel poorer because their 401K is going down, and now their houses are going down in value. In reality, it is not that they “feel” poorer, they are poorer. This is a “reverse wealth effect.”

The election was disappointing as no strong rebuke was given to current failing policies. Gridlock is the best that can be hoped for.

Likely by next spring, if not earlier, a recession will be widely felt. Central banks will not be able to help much without jeopardizing their credibility to fight inflation, and gridlock will blunt fiscal stimulus.

By stimulating too much, for too long, central banks are likely to make the downturn worse than it otherwise would have been.