A Tough Year For Economists, A Great Year For Investors

It has been said, that if you could place all the economists in the world end to end, that would be a good idea. In that position, they might have been more useful than they were in 2023.

While it has been a wild ride, in 2023, in the end, it has been a good one for most investors but a bad one for economists and market prognosticators. This despite sharply rising interest rates and an economy that was widely predicted to slide into recession.

There is an old and accurate market aphorism: don’t fight the FED. But for much of the year, that is exactly what the market did, anticipating a “pause”, and then a pivot to rate cuts for much of the year. After the last FED meeting, bond futures have reacted in a way that suggests 6 or 7 rate cuts are already anticipated even though the FED remains on pause.

The stock market performance as measured by the S&P closed up around 26%. As good as it is, it closed out the year just about a half percent below the high of 2 years ago. Thus, on a two-year basis, the gains are not that impressive because we are almost at the same level as we closed in 2021.

But that does not detract from it being a very good year, especially with an economy that has struggled. If it had been a down year, the two-year performance would have been that much worse.

The market has been especially strong in the past nine weeks giving frequent breadth thrusts (lop-sided advances over declines with high volume). This has quite a few technical types looking for a very strong market going forward.

The performance certainly surprised most of us, especially professional Wall Street prognosticators. The year ended up 18% above the average Wall Street forecast, according to Charlie Bilello.

After a sharp pullback in October, the market had as mentioned an extremely strong closing for the year. This has left most momentum and sentiment indicators in overbought territory for over a month. While not a record, we are now about 10 days from the longest string of overbought days without a correction.

Valuations remained high and have gotten even more excessive, depending on what metric you decide to use. Since 2023 saw the passing of Charlie Munger, the second in command to Warren Buffet, we might use the valuation indicator most favored by the “sage of Omaha.” Buffet likes the relationship between the total market capitalization and Gross Domestic Product. The market cap is now 175% of GDP, which is the second-highest reading ever recorded.

So, we are more than just a tad more expensive than normal. Pick whatever indicator you like best: price to earnings, price to cash flow, price to sales…they all are high. Thus, the year could be described as an expensive market that got even more expensive.

As good as the S&P did, it was overshadowed by the tech-rich NASDAQ which closed up about 55%, more than twice the performance of the broad market. This is the best performance since 1999 which was achieved just before the “tech bubble” burst in 2000. It is worth noting that after that peak in ’99, the NASDAQ suffered a loss of 36% in 2000, a loss of 33% in 2001, and a loss of 37% in 2002.

History often shows a pattern of overperformance being followed by underperformance. There is a general proportionality at work in the market. The more excessive the upside, the sharper and more prolonged the correction of those excesses.

It has been observed that the most ominous market phase occurs when most investors believe “It is different this time.”

Clearly, the majority of investors believe that things are different this time. The FED has the means to keep the markets afloat, they intend to do so, and they will make things good for the coming election cycle. The market has shrugged off most of the traditional indicators such as an inverted yield curve, sharply declining money supply, contracting bank credit, weakness in commodity prices, a freeze-up in residential real estate, a serious slump in commercial real estate, and a near-record decline in both length and severity in the Leading Economic Indicators.

Historically, inflation does not come down unless there is a recession. Investors seem to be betting that this time it will be different. With so many traditional signals going haywire, we can see some justification for such optimism even though we remain skeptical.

Even bank failures in 2023 did little to rattle the market, nor did the plight of regional banks and their exposure to commercial real estate.

Liquidity it would seem, is now the paramount indicator. As long as there is lots of money sloshing around, it will gravitate to the stock market. And we mean the US stock market. Rarely if ever, have we seen the US market so expensive relative to foreign markets.

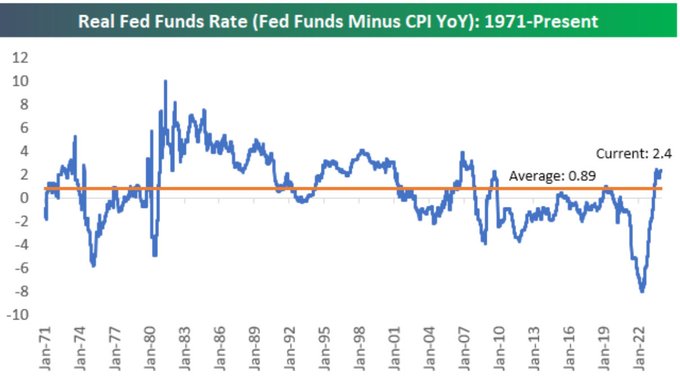

We read many analysts who say money is easy, and that is what is driving the market. Yet the chart above from Bespoke suggests real rates are well above average. Maybe money is readily available, but just expensive.

Avid bulls note that there are about $6.2 Trillion in money market funds just waiting to flow into the market. On the surface, that indeed seems huge.

However, some perspective is helpful. Back in 2018, just five years ago, there was “only” around $3 Trillion in money funds and so today’s balance seems so much more. The only trouble is that in 2018, the total market capitalization of the US market was around $21 Trillion and today it is slightly over $50 Trillion. In short, the cash on the sidelines, while massive, has to support a market that is more than twice as expensive as it was in 2018. The relationship of cash to the capitalization size of the market that it must move is not much different.

Also driving the market are the prospects of artificial intelligence and its promise to enhance productivity.

Those old enough to remember 1999-2000 remember the excitement about the internet. It was real to be sure, changing the way we interact with each other, the way we get news and music, the way we shop, even the way we bank. But while the technology did go on to prove itself, it still caused a boom and then a bust in the stock market.

Sometimes markets run up so fast, so far, they have already discounted both the hype and reality of technological change.

The hope of AI is that it will enhance productivity. Population growth plus productivity defines growth. With the former headed to zero or below, productivity remains the key.

Liquidity flows into index ETFs have been huge with the nation’s money managers putting the money to work in stocks. The National Association of Investment Managers as measured by the NAAIM Index now reads over 100%, which means managers are so confident they have spent their last dime and are now borrowing money on margin to get into the market. That is a high number for sure, but we have seen it higher in the 110% range or slightly more.

What could go wrong with that? A cynic would point out that the last time it read over 100 was last August, just before the nasty September-October sell-off. But maybe, things are different this time…or not.

It would seem there now is a very large camp that believes a “soft landing” (sharp reduction in inflation, falling interest rates without a recession, and thus avoiding a contraction in earnings) will be achieved.

There is another contingent, much smaller, that still believes that a recession is likely (hard landing). It was the consensus view last year but the recession never showed up. Those left stammering to explain themselves say the recession has been delayed by government stimulus but it will be forthcoming. You won’t get a substantial reduction in inflation and interest rates without a recession. We plead guilty to being mostly in this camp.

There is even a smaller camp that now believes in “no landing.” The economy is already turning up. Hardly anyone it would seem would be prepared for this contingency. If it happens, inflation will drop a little, but come roaring back. Interest rates will drop a little, and they will come roaring back. The fact that so few hold this view makes us nervous. Just as this year proved, the markets are always capable of fooling the vast majority of prognosticators. Could it be the FED has relented before the inflation dragon has been slain?

Speaking for ourselves, we don’t think stocks will do that well if interest rates don’t drop substantially, and what would keep them from dropping? The FED relenting too early on inflation and simply the gargantuan volume of government bonds that must be issued to fund staggering deficits could stop the decline in rates. Besides financing the immediate deficit, there is an estimated $8.1 trillion of government debt coming due in 2024 that must be refinanced. No landing could prove more problematic for markets than a hard landing because embedded excesses will not be wrung out of the market or the economy at large.

The next year is an election year. If the Democrats have proved anything, they will innovate and break all traditions and norms to win. Will the Federal Reserve maintain independence or act as a political arm of the Administration?

In our last report we shared our concern that the market is getting overheated and that while we expected (and we got it) a strong finish to the year, we did not think it would extend too far into January. Somewhere out early in Q1 of 2024, there is likely a sharp correction or worse.

The next few weeks will determine whether our view prevails or whether we are just as bad as the other Wall Street prognosticators. Maybe it is because of our age but we have always felt that if we had to face a trade-off between missing out on an opportunity or losing our capital, we would prefer missing the opportunity.

Why? Because if your capital is secure, you live to fight another day. Opportunities will come along again and we will be prepared to buy value when it is available.

For us, the market is too overheated and expensive to get aggressive at this point. We are not yet prepared to say this time it is different. Markets cycle from overvalued to undervalued. True, timing those moves is difficult but that doesn’t mean the cyclical nature of markets has been eliminated.

We were glad to participate fully in 2023 but we are nervous about 2024 and will take some of our chips off the table in early 2024. But that is just our personal opinion.

Leading the pack in terms of 2023 performance was Bitcoin, up about 154%.

Its extreme gyrations continue to demonstrate that it acts nothing like a stock (it has no earnings), nor like a currency. It is a privately issued something that consumes vast quantities of electricity. But for its believers, it made them big money.

Otherwise, it was quite a decent year, not just for stocks, but for other investments as well. Be grateful for that. Here is a short list of how the year went: Data is from Stockcharts.com and may vary slightly from other sources:

S&P was up around 26%. But the equal-weighted S&P, not so influenced by the “magnificent seven”, turned in a respectable 13.7%.

The smaller and mid-cap sector suffered, with the Russell 2000 dropping about 10.4%, and that was with a very strong recovery late in the year.

AGG or the bond average was up 5.55% so a stock-bond mixture did OK this year.

Gold bullion was up 14%, about the same as the equal-weighted S&P, but gold shares lagged again with GDX up about 10%. Silver lagged both, down about 1%. Gold shares are a real puzzle right now. They are roughly 50% undervalued compared to where they were several years ago when gold was above $2,000 per ounce. Cash flows are good, energy costs have moderated, and labor costs are no worse than other industries. Yet, they languish.

The CRB, an index of commodities was down almost 5% with West Texas Intermediate oil down almost 11%.

In terms of economic performance, there were also surprises. The Economist magazine looked at a combination of share price performance, employment change, GDP growth, and inflation measures and came up with these rankings:

Ranking first was surprise…Greece. It was then followed by South Korea, the USA, Israel, Luxembourg, Canada, Chile, Portugal, Spain, and finally Poland, as the top 10 economic performers.